NZFFA Member Blogs

Member Blogs

-

Brian Cox's Blog

-

Chris Perley's Blog

-

Dean Satchell's blog

-

Denis Hocking's blog

-

Dennis Neilson's blog

-

Eric Cairn's Blog

-

Grant Hunters blog

-

Hamish Levack's Blog

-

Howard Moore's blog

-

Ian Brennon's blog

-

Ian Brown's Blog

-

Jeff Tombleson's blog

-

John Ellegard's blog

-

John Fairweather's blog

-

John Purey-Cust Ponders

-

Murray Grant's Blog

-

Nick Ledgard's Blog

-

Rik Deaton's Blog

-

Roger May's Blog

-

School of Forestry blog

-

Shem Kerr's blog

-

Vaughan Kearns blog

-

Wink Sutton's Blog

Recent blogs:

An eight Bullet Point summary of why the "Jones formula" to make NZ sawmilling great again is doomed to failure

Dennis Neilson's blogWednesday, June 03, 2020

Some reasons why Minister Jones’ attempt to re-direct some or all of the ~20 million cubic metres per year of export logs to domestic sawmills to process more sawn timber and create more jobs -- is doomed to failure

- Only three sawmills of 60 in NZ (Red Stag Rotorua, CHH Kawerau and CHH Nelson), working even part-weeks, can over-supply the entire NZ market for sawn timber. This over-supply will get worse (a lot worse), as annual NZ housing starts reduce from 37,000 in 2019 to between 11,000 and 20/25,000 in the next 12 months (BNZ prediction). One other very experienced observer said today, “NZ sawn timber demand will likely halve over the next 3 years compared to 2019.” And last night it was predicted that Australian housing starts will fall from 160,000 to 110,000 per year

Other (smaller) mills producing for the NZ market only make the oversupply worse. And, once a huge expansion to one of these three sawmills mills (CHH Kawerau) is complete the oversupply situation will get even worse.

- NZ sawmills cannot export structural housing timber to Australia, as almost no NZ pine timber can meet Australian building timber stiffness standards ( MGP10 & MGP - e.g. MGP10 indicates a minimum threshold for stiffness properties of 10,000 MPa). So 70% of total Australian wood demand is out of bounds to NZ exports. As a result of changes to the Standards and European competition, NZ sawn timber exports to Australia have fallen by 75% from 2000 to 2018.

- In the last 10 years while governments in Russia, Europe and latin America have subsided the building of dozens of huge new sawmills and other mills costing $10s of billions, the undercapitalised and non-subsidised NZ sawmilling sector has languished. While being in the top quartile of global scale and efficiency in the 1980s, it has “fallen off the cliff” to be in the bottom quartile globally (with two of 60 mill as exceptions). European sawn timber shipments to Australia have increased by more than 500% from 2000 to 2018 - the biggest single “nut-crusher” of the NZ timber export industry. All this Pinus sylvestris (Scots pine) and Picea abies (Norway spruce) timber meets Australian Standards.

- NZ sawmills have not been able to find a single cubic metre of extra export sawn timber market volume in the last 18 years - in fact it has found less from 2002 (1.835 million m3) to 2019 (1.821 million m3).

And it is only going to get a whole lot harder in the face of recent huge increases in global sawmilling capacity**, and into a massively over-supplied global sawn timber markets.

** Extra new annual sawmilling timber capacity being built in Central Europe alone between 2020 and 2022 will be as much as the total NZ timber export volume. Ditto in Russia (and much more). Ditto recently/now/soon in the US South -- so much that two huge new sawmills (Klausner in NC and FL) have just gone bankrupt.

FOR THE ABSENCE OF DOUBT: For every 1.0 cubic metres of new export timber market the NZ sawmilling sector has found since 2002, it has lost another 1.01 cubic metres.

- A plethora of inefficient, high cost, over-manned, low technology mills, made worse by the incompetence of many NZ sawmill owners, managers and advisors have resulted in the failure of 55 sawmills in the last 16 years. The details can be seen here

Chinese sawmills are 15-20% more efficient than NZ sawmills by conversion from log to timber (which equates to twice the profitability than NZ sawmills); and up to five times better by conversion from log to plywood.

- For the NZ sawmilling industry to be internationally competitive, the 60 existing mills must be replaced with <10 big new automated ones, with a loss of at least 75% of existing sawmill jobs.

- NZ mills cannot increase exports of plywood or Laminated Veneer Lumber (LVL) against vicious and increasing competition from Chile, Russia and Europe. NZ exports of plywood and LVL have fallen by 70% in from 2005 to 2018 -- which forced the closure of one plywood/LVL mill in 2018 (Juken in Gisborne) and soon 70% of one LVL mill in 2020 (CHH Whangarei).

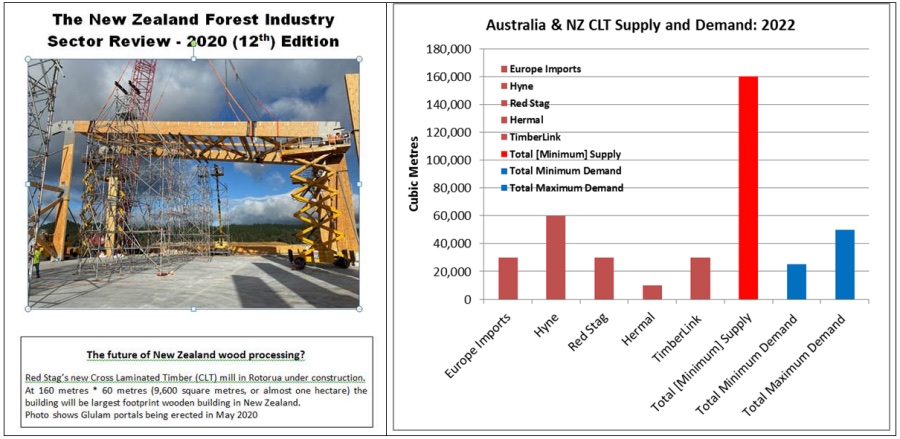

- The Minister talks about the new “wonder product” of Cross Laminated Timber (CLT). But CLT is already over-supplied in Australasia, which caused the closure of NZs only CLT mill (Nelson) in 2018.

Once the new Red Stag CLT mill is commissioned in 2021 (see below), with more new mills in Australia (and the massive expansion of CLT capacity in Europe -- by 20 times Australasia’s demand), the NZ + Australia oversupply will be savage, chronic and permanent. Trans-Tasman CLT production capacity alone in 2022 will be 3 to 7 times demand (see chart below).

Any new entrant in NZ making CLT would be instantly crushed by the competition. See below DN estimate of 3 June 2020.

Ask the NZ Wood Processing and Manufacturing Association (NZ WPMA) -- and/or any advisors/specialists/experts at MPI or Scion to analytically unravel any/all the above with their own version of “facts”. I hope they can. I sincerely hope they can.

Discussion points for a meeting with Dr Rod Carr, Chairman of the Climate Change Commission

Howard Moore's blogTuesday, January 21, 2020

As a new item for my blog, I offer a briefing paper that Hamish levack, Egon Guttke and myself gave the Chairman of the Climate Change Commission prior to a meeting with him last week. We covered a little more ground than this, but these were the highlights.

In October 2015 New Zealand finalised its NDC target of reducing greenhouse gas emissions to 30% below 2005 levels by 2030. The target is equivalent to an 11% decrease below 1990 levels and represents a progression on our target for the period to 2020 (which was -5%).

Accelerated afforestation and complete restocking after harvest will help New Zealand achieve this target. However in order to count, new forests have to be planted on grassland. Only farmers own grassland. To minimise social conflict, rather than sell that land for afforestation, the farmers should plant it themselves.

The NZ Farm Forestry Association represents people who have made this choice.

Small grower / large grower distinction

There are over 14,000 small forest owners in NZ with commercial forests of between 5 and 1,000 ha. Altogether they own around 500,000 ha, which is a third of the national estate. Roughly 200 large forest owners hold the balance.

Nationally our Association has over 1,400 fully paid members, but a much wider constituency. Our email list is over 3,500 and our postal addresses list is over 10,000 (roughly two thirds of all forest owners).

Most small forests were planted during a five-year window of speculation from 1992-1997 when export log prices were extraordinarily high. In general the owners all have day jobs, i.e. forestry is an investment rather than a primary activity or source of income. Their forests have few age classes; their knowledge of forestry is limited; and their demand for skills is sporadic.

In contrast, most large forests were first established before 1990 and are run by professionals as full time businesses. Consequently while the two types of forest owners have much in common, they are widely different. Their interests are further separated by the ETS, where small growers’ post-1989 forests can earn carbon credits but large growers’ pre-1990 forests cannot.

Small growers’ ‘wall of wood’

Because small forests were largely planted in one burst of activity in the 1990s their harvest is starting to create a ‘wall of wood’. Small growers are contributing an increasing share of the income of the Forest Growers Levy Trust. NZ Farm Forestry members represent these growers on the official committees that recommend how this industry levy is spent.

There are several important features about this ‘wall of wood’.

- Although most small forest owners could have registered in the ETS, many did not. This means they are free to change land use without penalty. Others who did join are holding NZUs for exactly this purpose.

- Some growers who have been disappointed with their forestry returns have already converted their land back to pasture.

- A second rotation forest generally makes more money than a first rotation one because all the roads have been paid for. It makes more sense to replant a harvested block than to plant fresh grassland.

- Accordingly, we should be doing all we can to encourage replanting. This includes improving the harvest outcomes for small forest owners.

- If we want to add national processing capacity, and taking replanting into account, new commercial forests should be spread by location and age class to smooth log supply.

- Whether or not small growers replant, harvesting their forests will contribute to gross emissions over 2020 - 2030.

Views on new planting

The national commercial forest area fell in the early 2000sreflecting land use change from forestry to pasture, mainly in Canterbury and the central North Island. New plantings by late 2018 totalled 9,100 ha, compared to 30,000 ha in 2001. The lowest point for new plantings was in 2009 with only 1,900 ha planted. The areais currently 5% down from its peak of 1.83 million hectares in 2003 and high land prices discourage further large-scale expansion.

Australia’s wild fires have implications for the increasingly warm and dry parts of New Zealand. In these areas the risk of fire on top of restrictions on land use by many Regional Councils discourages investment in both replanting and afforestation.

While members of the Farm Forestry Association and our wider constituency own and have the capacity to increase areas of native forest, this is typically ten times more expensive to successfully establish and twenty times slower to grow and fix carbon.

We would like to see

- Stronger border controls for biosecurity. Pathogens exist that could devastate our radiata pine plantations, making it very difficult to meet our climate change targets.

- Stronger rural fire prevention campaigns and fire fighting capacity. Climate change means rural fires will inevitably increase in frequency and severity.

- Free education about forestry investment and associated ‘best practice’. If the public does not understand forestry it will oppose any expansion.

- Less emphasis on planting indigenous forest and more on planting fast growing species. Managing diversity is nice but managing climate change is urgent.

- The price of NZUs to rise to a level that encourages an increase in net stocked forest area, preferably by farmers planting some of their own land.

- Public approval of gene editing allowing Scion to increase the rate of carbon sequestration. Business as usual is over.

Disclaimer: Personal views expressed in this blog are those of the writers and do not necessarily represent those of the NZ Farm Forestry Association.