Risk management and insurance

Keith Hales, New Zealand Tree Grower February 2005.

This is the first of a two part series of articles on risk management and insurance. The next article will address insurance, but before considering spending money insuring your trees you should go through the risk management process.

Insurance is only one of the parts of the total subject of risk management and it is also just one of the ways through which you can get the money you want to reinstate a loss. Before you commit yourself to any insurance, its worthwhile thinking about how the insurance fits with the risks you face. There might be a cheaper and just as safe way to get the same result.

So before we can consider insurance in general, or trees in particular, we need to have an understanding of the theory of risk management.

Managing risk

Risk management is not some new technique dreamt up by consultants through which they can earn lots of fees. In fact the theory became formalised in the 1930s when someone decided that what we had all been doing instinctively might be done better if it had some rules attached to it.

As you read on, bear in mind that although it is convenient to talk about risk management as having steps, each step of the process is inter-reactive. If you do something that causes a change in one step then there is most likely to be a knock-on effect on the other steps. In fact it is better to visualise the process as a circle of steps instead of a simple column.

What do you want?

It is most important to first decide what you want if a loss happens or a risk is realised. The reply might be that you want enough money to pay for the entire loss so that you are put back financially into the same position as you were before the loss. But you might select an opposite extreme and say that you only want enough to pay for the cost of clearing up and walking away. The main thing is that you should make a conscious decision about what you do want, because whatever you decide is going to have a big effect on the next steps.

Risks

Risks fall into two very convenient categories.

One group of risks can, if they happen, only cause a loss and generally these risks can be insured – they are known as the insurable or static risks. Examples of static risks for trees would be fire, storm, flood, lightning, disease, infestation, drought and all the resultant costs, as well as liabilities to others caused by physical negligence, advice or liability at law.

The other group of risks are known as financial risks and their distinction is, when they happen, that they can cause either a loss or a gain. Financial risks are not generally insurable but financiers have some methods through which loss can be covered.

Examples of financial risks are currency fluctuation where bankers will provide hedging cover against this risk, loss or gain in product pricing due to market fluctuations, failure of the market place or changes in the law.

You can use the principles of risk management to manage any form of risk but we are only going to look here at the static and insurable risks.

Risk identification and analysis

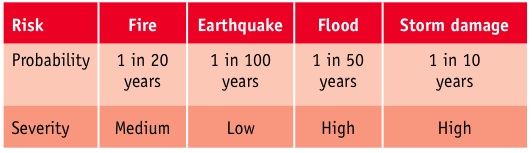

The first step then is to think about and then make a list of the risks that you face. You can go as wild as you like as you can always cull the list later on.

What you are now going to do is to consider how often a risk might happen, and then if it does happen, what could be its worst cost. Add a couple of columns alongside the list of risks and head them probability and severity.

Now divide each of the columns into three and under the probability column put down some time scales such as once in a year, once in 10 years and once in 100 years. Under severity put down some costs on an ascending scale. The first should be an amount that you can afford to loose without hurting at all, the next should be a number that hurts and will mean that you might need to borrow to recover, and the last one is if this cost happens then I will just go under.

Everything about this process is individual and subjective so there will be no set pattern.

Depending on how refined you want the probability analysis to become, you might employ experts such as fire engineers, seismologists, meteorologists or actuaries. But most analysis can be done by just using good old common sense.

It is likely that when you have done this exercise you will have a list of risks which have an ascending level of cost effect. The majority of your risks will probably have a low to moderate cost – only a few will be very expensive.

As you go through this exercise do not be tempted to write off a risk because it is too remote. They thought before September 11 that there was no probable event that could cause the loss of both towers of the World Trade Centre.

Reducing the severity of risk

So you now have a good list of what might go wrong and how often you think it could happen, and if it does happen, what it might cost.

The next step is to consider whether there are any physical or managerial systems that could be put in place that will reduce the severity or probability of a risk. For example, if you break up plantings into smaller blocks with secure fire breaks, then the cost of a fire cost will reduce. As you consider this step make sure that you do not become a slave to risk reduction. The idea is to try to ensure that risks are reduced but with an eye to overall economics.

Funding

This is where we talk about the life raft that you might create and have available if the big ship sinks. There are many forms that the life raft might take.

It needs to be remembered that there are only two sources from which money will be available to pay for a loss. The risk management jargon for one source is internal and for the other is external.

Internal sources are those that you can access without having to deal with someone else. In other words you could draw down from a fund that has been built up for the purpose or just take the money from cash flow, or just perhaps reduce the value of the investment. If the loss is suffered by a large company an option is to issue more shares or asking the shareholders for more money. External sources are by borrowing from a financier, from the liability in contract with someone else or from the proceeds of insurance.

Obviously there is a cost attached to getting cash out of an external source so, unless the external arrangement has a proven economy, the more that can be obtained internally the better.

Putting it all together

In the risk analysis that you did you should look for any risk that has a high degree of probability because losses, however expensive, that are caused by a risk that happens very regularly should be funded internally.

Formal risk management is mostly common sense and you will probably now be saying that is exactly what I do already. I buy insurance and I only buy for a sum insured that I think would be the maximum that I can lose following the worst risk event, and I bear the first part of any loss through an excess. More on this topic of insurance will be in the follow up article in the May Tree Grower.

Keith Hales of Risk Management & Insurance is a risk management consultant based in Wellington